Public contracts as a pathway to financial inclusion: lessons from the CREDERE pilot

For small businesses such as software support providers, geophysical mapping companies or even farmers, winning a government contract can be a turning point. In Colombia, almost half of small and medium-sized enterprises (SMEs) that secured government contracts experienced significant growth beyond their initial contracts.

Public procurement, when it works, is one of the most powerful instruments of economic inclusion for a government. In Brazil, small firms that win public contracts grow measurably, and most of the new jobs they create go to people who had never held formal employment before. Similar trends are visible in Africa: in Kenya, targeted procurement policies that reserve 30% of contracts for disadvantaged groups have doubled participation among women-owned businesses. When SMEs can access public contracts, the benefits extend well beyond individual firms to broader economic inclusion.

But when it doesn’t work, it does the opposite. SMEs win contracts they don’t have the working capital to deliver. They borrow on punishing terms, sometimes from informal lenders, to buy materials or pay workers up front. When the government pays late, as it routinely does, the interest eats the margin and then the business.

Sitting between these two outcomes is a strange failure of the financial system. With the customer being the state, the receivable is verifiable, and the risk should be among the lowest in commercial credit. And yet financial institutions don’t see it that way. The SMEs who win these contracts are routinely treated as too small, too new, or too informal to qualify for the working capital they need to deliver on the work the government just hired them to do.

From 2022 to 2025, with support from the Mastercard Center for Inclusive Growth and Caribou Digital, we set out to test in Colombia whether open contracting data could change that.

This is what we learned, what surprised us, and what needs to change to ensure small businesses succeed.

What we set out to do

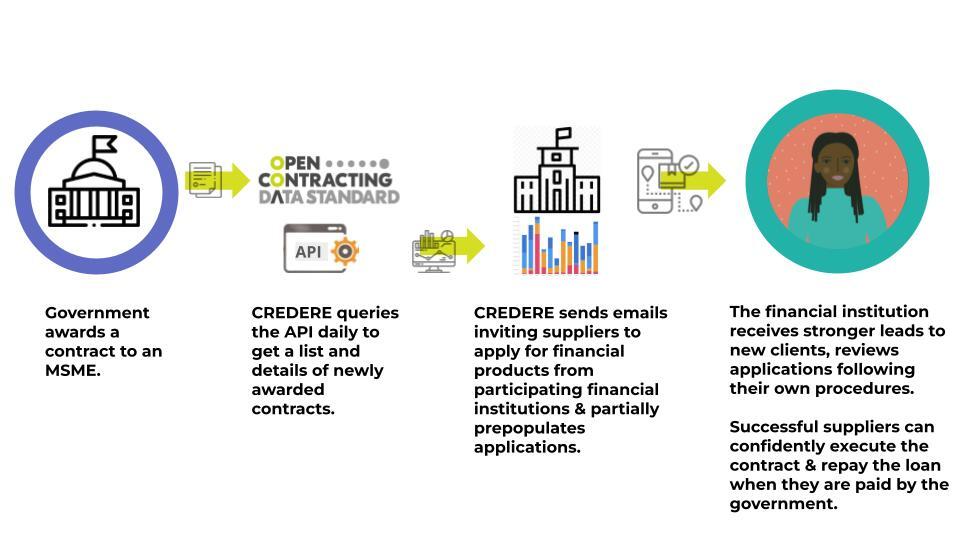

At the core of our pilot was a digital solution we called CREDERE, designed to sit between government, small businesses and financial institutions. Our theory of change was straightforward: if financial institutions could see verified, timely data on awarded contracts, they could more confidently offer financing tailored to SMEs’ procurement needs.

Every day, Colombia’s procurement agency, Colombia Compra Eficiente, publishes contract awards as open data. Our software collects that data, identifies the SMEs that won, and emails them an invitation to apply for a credit or a contract-backed financing mechanism through a participating financial institution. Most of the application is pre-filled using the contract data itself. The SME uploads what’s missing, submits, and the financial institution reviews the application through its own process.

The pilot ran in stages. We started with user research and design alongside SMEs, financial institutions, and the city of Bogotá and built the software. Launched first in Bogotá with two financial partners, Clara and Escala Capital, we then scaled nationally. We refined the platform based on what SMEs and financial institutions told us and worked toward a sustainable operating model. By the time the grant ended, two more financial institutions had committed to joining.

Since the beginning of Clara’s collaboration with CREDERE, we have identified a great opportunity to expand our financial solutions, focused on simplifying and enhancing payment management for companies throughout Colombia. Due to its high volume and scope, public procurement presents a major opportunity for companies to not only optimize their operations but also drive their growth with greater agility and transparency.

What we achieved

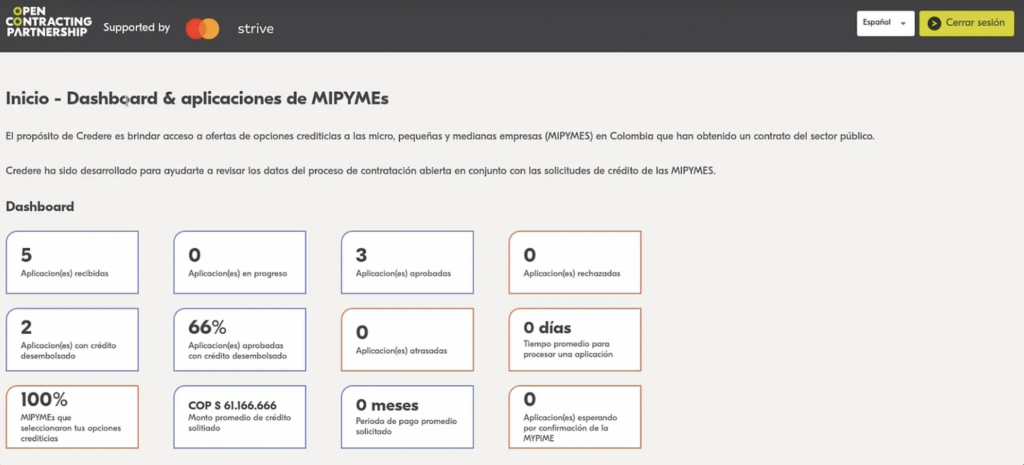

CREDERE reached 12,464 SMEs, about 47% of all small businesses awarded public contracts in Colombia in 2024. The other 53% had missing emails, incomplete contract records, or no business identifier we could use to find them. What we measured was the demand we could see. The actual demand is almost certainly higher.

Among the SMEs we reached, engagement and application rates exceeded our expectations, and 31% of the SMEs who engaged were women-led. These results confirmed that contract-winning SMEs want financing tied to the contracts they’ve won, and that they’ll act on it when given the chance.

By the time the pilot ended, we had disbursed roughly US$234,000 in financing to 56 SMEs, including around US$131,000 to women-led businesses.

We have been working in public procurement for a long time. We have witnessed first-hand how critical it is for the public procurement market to function well in order to deliver critical public services such as school meals. In this context, it is important to empower all the actors involved and ensure they have the appropriate financial services to efficiently fulfill the contracted services. CREDERE allowed us to reach new clients and expand financial services to SMEs.

What open data made possible, and where it fell short

One of the clearest lessons from the pilot is that open contracting data can meaningfully lower the first barrier to financial inclusion: visibility. CREDERE reached nearly half of all SMEs awarded public contracts in Colombia in 2024. Engagement and application rates exceeded expectations, signaling strong latent demand for financing among contract-winning SMEs.

This was made possible because Colombia Compra Eficiente publishes structured open data from its national electronic government procurement platform that includes key data fields. For example, Colombia disaggregates both women-led and small and medium-sized enterprises, enabling us to apply a gender lens to the project. The data also included contact information for the suppliers, enabling CREDERE to automatically contact them by email.

At the same time, the pilot exposed how fragile this pathway becomes when data quality is uneven. Less than half of the awarded SMEs had sufficient, reliable contact information or business identifiers to be reached through the platform. Missing emails, incomplete contract records, and inconsistent identifiers directly constrained inclusion. This reinforced an important insight: open data is not just about transparency. Open data is infrastructure, and weaknesses in that infrastructure have real downstream effects on market participation.

Financial inclusion is a systems problem

Another critical lesson was that access to finance in public procurement cannot be solved by a single financial product, or even a single type of financial institution. While FinTech partners proved agile and willing to experiment, their offerings often targeted more formalized SMEs or larger contracts. Traditional banks, on the other hand, had broader product portfolios but struggled to adapt rigid internal processes and systems to a digital, data-driven model.

Unfortunately, most financial institutions do not yet systematically recognize public contracts as collateral. The value of CREDERE for them was to connect them to a pool of “quality” potential clients on the logic that if they are robust enough for public procurement, they should be creditworthy. There was a structural gap that the public contract itself was not factored into the creditworthiness. And according to the Small Firms Diaries research project, even formalized firms in Colombia struggle to access the finance needed for working capital from financial institutions. A small minority of financial institutions are beginning to consider procurement information in their assessments, but their processes remain manual and labor-intensive, with significant opportunities for digitization and the use of open procurement data to improve efficiency.

Both SMEs and financial institutions pushed us to do more than the platform was designed to do. SMEs asked whether CREDERE could help them secure pre-approved financing before bidding, to attach to a tender as proof they could deliver. Others wanted help once a contract was underway, tracking delivery and payment. Financial institutions raised similar requests. The appetite for tooling in this space clearly extends well beyond the moment a contract is awarded.

There is a role for a tool like CREDERE to play a catalytic role in the ecosystem by an actor, such as OCP, who knows what is possible through developing digital data solutions and who understands the barriers and opportunities of the public procurement process.

Trust, incentives, and achieving scale

The pilot underscored that financial inclusion through open contracting is as much about relationships as it is about technology. Onboarding financial institutions required navigating legal, compliance, credit, and product teams, often over many months.

Lead quality mattered more than lead volume. Financial institutions tended to ask for as many leads as a platform could send, but what actually changed their behavior was the quality of those leads. Pre-screening before referral, using credit bureau data or public business registries, would deliver fewer applications but a much higher conversion rate. That trade is almost always worth making, and it’s also what builds the relationship of trust between platform and lender that everything else in this work depends on.

While interest from additional banks grew as CREDERE demonstrated its ability to deliver high-quality leads, most institutions required longer pilots and clearer revenue signals before committing.

Open contracting as an opportunity to generate leads and increase financial inclusion

After the conclusion of the grant, CREDERE is currently offline. Although the pilot didn’t reach financial sustainability, it clarified viable pathways forward to scale and sustain this initiative over time, including onboarding larger institutions, refining pre-screening to improve application quality, and transitioning to a locally operated, commission-based model.

The results reinforced several broader lessons for the open contracting and financial inclusion communities:

- Open contracting data can act as a powerful market signal, but only if it is timely and usable.

- Financial inclusion in procurement is a systems challenge, requiring coordinated changes across data quality, financial products, institutional incentives and SME support.

- Digital platforms can reveal demand, but they cannot substitute for product diversity or regulatory and risk-model innovation within financial institutions.

- Sustainability depends on scale and trust, both of which take time to build.

We also recognize that CREDERE may function better as a lead generation tool for financial institutions rather than as a marketplace. We would also like to embed procurement data directly into financial institutions’ underwriting, alongside other risk signals and a firm’s track record on past contracts. This would give banks a richer picture of the SMEs, so they can build credit products tailored to this segment.

Perhaps most importantly, the pilot demonstrated that open contracting is not just about accountability or efficiency. It can be a pathway to economic inclusion, helping small businesses around the world translate public market access into real economic opportunity.

Reach out to us if you would like to discuss replicating this model.